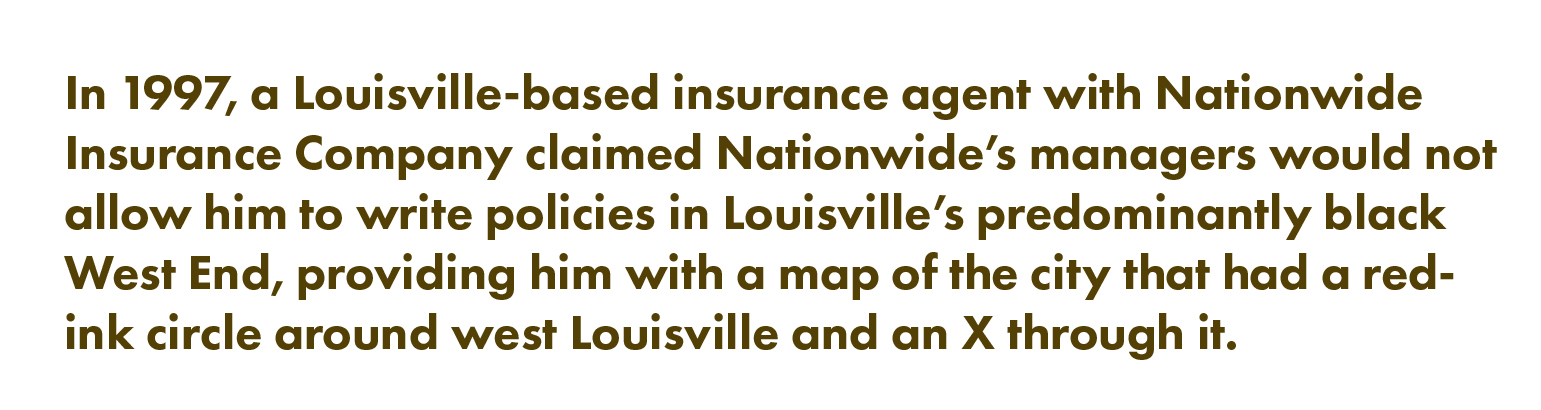

A sliver of yellow exists in red Russell. It’s right along Chestnut Street, where a Black middle class thrived. It’s the only predominantly Black area that received anything but a D-grade. “The area is . . . occupied by negroes and consisting of improvements of better type than those surrounding.” Surveyors touted its proximity to schools and churches. (The strip was demolished in the early ’60s.)

Poe uses 2010 census data (the latest available at the time of his research) to show how redlined neighborhoods stack up now. Russell, Portland and Smoketown all have poverty rates above 40 percent. (Areas around Shawnee and Chickasaw Park that were graded better have lower rates of poverty.) Vacant and abandoned homes plague the redlined areas in greater numbers. Poe also looked at mortgage denials between 2011 and 2013 and found that 41 to 75 percent of mortgage applications were denied in certain areas of Russell and Portland. Smoketown and Shelby Park had a mortgage denial rate of 21 to 31 percent. Out east — Indian Hills, the Highlands, St. Matthews — the rate was 10 to 20 percent.

None of this shocked Poe. But it did unsettle him. “There was a systemic effort to abandon (certain) neighborhoods,” he says. “Redlining became systematic in real-estate market analysis. We don’t call it that. But when we do real-estate market analysis, there’s a demographic study within that.” He uses an example of a grocery store. If a grocery doesn’t like the demographic study of a neighborhood it’s scouting? “It doesn’t build a store there,” he says.

A half-dozen west Louisville baby boomers reunite over strong coffee and homemade ginger cookies. A few minutes in, it’s a loose thread of happy memories — We lived in that pink little house after you! I used to sit in my tree house and watch the horse races! There were so many officers on my street we called it the 41st Street precinct! You remember when Southwestern Parkway was called Black Hollywood?

Everyone grew up in or near the Westover subdivision, now Chickasaw, a part of west Louisville that sat near a horse track, the old fairgrounds and a Ford plant. The group, which includes Metro Councilwoman Cheri Bryant Hamilton, has assembled at Leborah Goodwin’s house on Plato Terrace to talk with me about the effects of redlining on African-Americans. I was expecting sour tales of their parents struggling to purchase a home. I was wrong.

Lynn McCrary, a tall, outgoing woman with gray hair that sits like a crown, pulls the original deed to her parents’ home out of a tote bag — a tote, I might add, that’s an impressive archive of deeds, insurance papers and brochures from Martin Luther King Jr.’s visits to Kentucky. She passes the deed around.

“There’s my granddaddy’s name!” Carol Ray Bottoms exclaims, gleefully. Her grandfather — Joseph Reynolds Ray Sr. — was a prominent banker and real-estate developer who helped Black families purchase homes. (President Dwight Eisenhower appointed him assistant to the administrator of the Housing and Home Finance Administration.) Bottoms’ grandfather helped McCrary’s parents buy a home on Grand Avenue in May 1946.

“Get the court case!” Hamilton instructs.

Goodwin makes copies of a Court of Appeals decision from 1943 and hands them to the group. The case stems from a 1939 dispute. Joseph Ray was among a group of developers interested in building homes on land they had purchased near Chickasaw Park. Whites in the neighborhood fought to prevent it.

Hamilton reads out loud from the decision: “When questioned, Mr. Ray stated for the past 15 years the colored people of Louisville have been faced with the problem of new and better homes. Despite the fact that several thousand new FHA homes have been built in and around the city, less than 50 are for colored. The reason being that suitable locations could not be obtained. The acquiring of Westover subdivision . . . seems to be a partial solution to the problem.” The ruling goes on to say “no shacks, but only respectable types of homes will be built as a credit to the colored people and to that section of the city.” A victory.

“Wow,” somebody says. The room seems to sigh.

The group remembers other businessmen who helped Black families buy homes and raise kids who went on to become lawyers, judges and councilmembers. “This is like Hidden Figures!” Goodwin exclaims, referring to the recent film about the unrecognized African-American female mathematicians who played a pivotal role during the early years of NASA.

But discrimination lived. Bottoms, an elegant woman with a bob hairdo and stylish glasses, recalls helping her grandfather and father in the real-estate business. “I used to fill out the contracts, that was my job, and I remember a family, they both were teachers and only had one child, and I remember doing a letter that said they would not have any more children if they could secure a loan,” she says. The room murmurs another “wow.” “I typed a letter and I think my daddy scribbled some doctor’s name on it and we said she wouldn’t have another kid.” (Bottoms says the woman did end up having another child years later.)

Many in the room detail a resistance, a way around barriers to homeownership. Mammoth Insurance Company and Domestic Life and Accident Insurance Company, both Black-owned businesses on lively Walnut Street (then dubbed “Louisville’s Harlem” and now Muhammad Ali Boulevard), provided home insurance. “They (also) held a lot of loans for people’s houses,” Bottoms says. “People may not realize that, but they were the mortgage holders on a lot of the houses.”